- Home

- About Us

- Research

- Research Areas

- Agriculture

- Air Pollution

- Climate Change

- Economy

- Education

- Environmental Law & Justice

- Energy & Electricity

- Federalism

- Governance, Accountability & Public Finance

- Health & Nutrition

- Indian Politics

- International Relations & Security

- Jobs

- Land Rights

- Sanitation

- Social Justice

- State Capacity

- Technology

- Urbanisation

- Water

- Miscellaneous

- Research Initiatives

- Research Areas

- Publications

- People

- Events

Highlight>

Where is food inflation headed?

June 25, 2021

Price increases have been largely in imported items like edible oils and pulses. There is no generalized food inflation yet only because of subdued demand conditions.

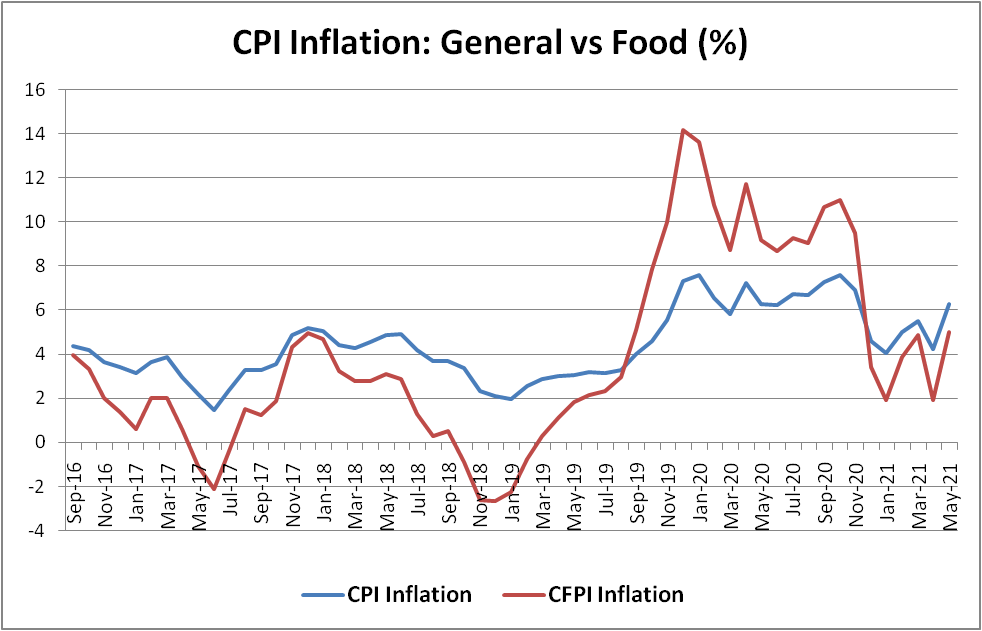

Low inflation, particularly in food items, was a significant feature of the Narendra Modi government’s first term in office. Annual Consumer Price Index (CPI) inflation averaged 4.3% during that period from June 2014 to May 2019. It was even lower, at 3.3 %, for the Consumer Food Price Index (CFPI) inflation. There was also an extended period, from September 2016 to August 2019, when the CFPI inflation rate ruled below general CPI inflation in each of those 36 months.

The Modi government’s second term has been different by contrast. Between June 2019 and May 2021, average annual CPI inflation has been 5.7%, while even higher, at 7.4%, for CFPI inflation. The chart below captures these trends. In combination with retail prices of petrol, diesel and LPG rising since June 2019 – from Rs 71.73/litre, Rs 66.51/litre and Rs 712.5/cylinder to Rs 97.76, Rs 88.30 and Rs 809, respectively in Delhi – it is clear that both food and fuel inflation have returned (Just for comparison: On May 31, 2014, petrol retailed at Rs 71.41/litre, diesel at Rs 56.71/litre and LPG at Rs 414/cylinder).

Source: National Statistical Office.

Much of the above inflation is imported, which is most obvious in fuel. Between May 2020 and May 2021, the average price of crude oil imported by Indian refiners has more than doubled from $30.61 to $66.95 per barrel (Brent has since breached the $75/barrel psychological level). This has, however, also been exacerbated by the Modi government hiking the excise duty on petrol and diesel by Rs 13 and Rs 16/litre, respectively during March-May 2020.

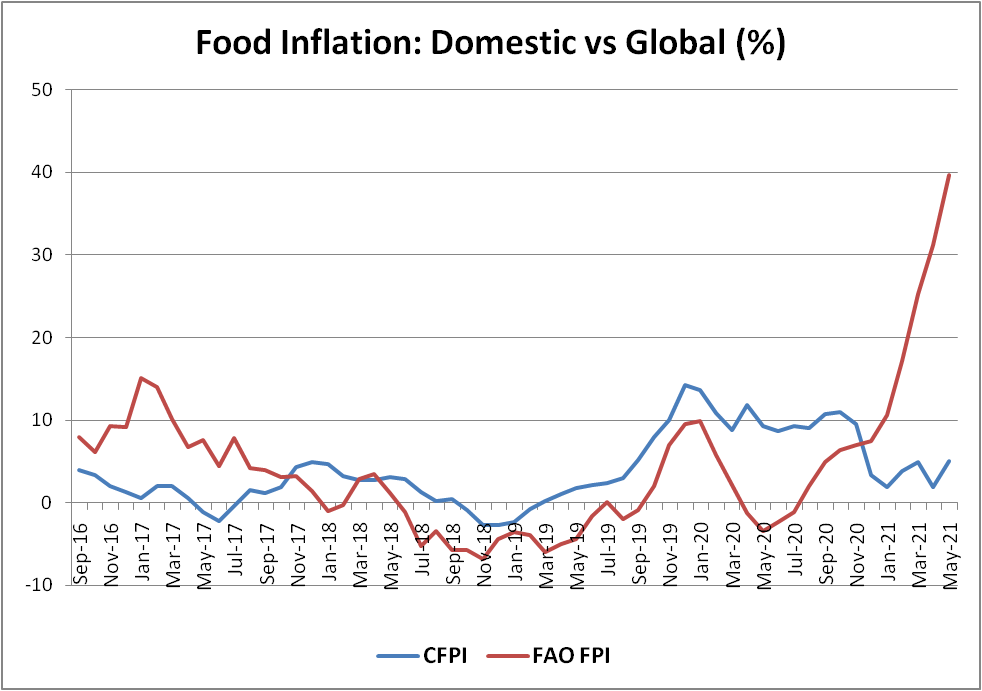

In the case of food inflation, too, the fall during the Modi-1 period was substantially enabled by international prices. Between May 2014 and May 2019, the UN Food and Agriculture Organization’s (FAO) world Food Price Index (FPI) dropped from 121.3 to 94.2 points (base year 2014-16=100). The global FPI inflation rate, however, started climbing from October 2019. That was roughly when domestic CFPI inflation also crossed the 5% mark for the first time in over three years. Both global and domestic food inflation saw an uptrend till February 2020, before the novel coronavirus pandemic struck. There was a divergence thereafter. The FPI inflation crashed, even as CFPI inflation remained at near double digits till November.

India’s food inflation began easing with the harvesting of the post-monsoon kharif crop, interestingly, when a recovery in global food prices was gathering steam. The FAO-FPI inflation started soaring from around October, as demand returned with economies unlocking and restoration of supply chains taking time. Dry weather-induced production shortfalls in Brazil, Argentina, Ukraine, Thailand and even the US, along with Chinese stockpiling, added fuel to the fire. The FAO-FPI hit 127.1 points in May 2021, its highest level since September 2011. On the other hand, retail food inflation in India, even at 5% in May, was way below the corresponding global rate of close to 40% (see chart below).

Source: National Statistical Office and FAO.

The impact of surging global prices on domestic food inflation has been largely on commodities that India significantly imports. The country annually imports 13-15 million tonnes (mt) of edible oil and produces only 7.5-8.5 mt. In pulses, domestic output has gone up from 15-16 mt to 22-23 mt in the last five years. While imports have also halved to 2.5-3 mt, they do still exert considerable influence on domestic prices.

The table below shows that edible oil and pulses are the food items to have registered the highest price increase in the last one year. At the same time, cereals, sugar, milk and even staple vegetables (potato, onion and tomato) have recorded little or no inflation.

All-India Modal Retail Price (Rs/kg)

| Year ago | Current | |

| Mustard oil | 120 | 160 |

| Soyabean oil | 100 | 160 |

| Sunflower oil | 110 | 175 |

| Groundnut oil | 145 | 180 |

| Palm oil | 85 | 135 |

| Chana dal | 60 | 80 |

| Tur/Arhar dal | 95 | 110 |

| Urad dal | 100 | 110 |

| Rice | 28 | 30 |

| Wheat | 27 | 22 |

| Milk | 46 | 46 |

| Sugar | 40 | 40 |

| Potato | 25 | 20 |

| Onion | 20 | 25 |

| Tomato | 20 | 18 |

Source: Department of Consumer Affairs.

The reasons are two-fold. The first is that these are foods predominantly produced domestically. The good monsoons in 2019 and 2020 – India, Australia and Canada were the only top agricultural powerhouse countries that did not face serious weather-related issues – have ensured no supply shortages in their case. The second reason has to do with the collapse of demand from successive Covid-triggered lockdowns. With hotels, eateries, sweetmeat shops, hostels and canteens either shut or operating at low capacity, apart from no wedding receptions and other public functions, food demand has been confined mostly to households. Even household consumption has probably been affected because of incomes taking a hit from the reduction in overall economic activity.

Simply put, while food inflation has made a comeback in India, it is not yet generalized in terms of sustained across-the-board price increases, of the kind witnessed during the previous United Progressive Alliance regime’s second term from 2009-10 to 2013-14. As of now, inflation is only in imported food items.

There are three factors that would influence the course of food inflation in the coming months. The first is international prices. The FAO’s benchmark index is now at a near-decade-high. It must be noted, though, that the same index, only a year before (May 2020), had plunged to 91 points, its lowest in four years. Whether the current global price surge is a pointer to a renewed “commodity supercycle” or simply a result of temporary supply-side disruptions remains to be seen.

The table below shows that global prices of all major agricultural commodities have risen considerably over last year. But they have also fallen off their peaks, which were mainly reached in May and reflected in the FAO price index for that month. The decline from the peaks is visible especially in palm and soyabean oil. That should, in turn, have some salutary effect back home. Cooking oil is the one item that has been really on fire in recent months!

International agri-commodity prices

| Unit | Current | Year ago | Recent peak | |

| Wheat | Cents/bushel | 652.00 | 485.75 | 761.75 (May 7) |

| Corn | Cents/bushel | 653.25 | 324.25 | 735.25 (May 7) |

| Soyabean | Cents/bushel | 1371.25 | 870.75 | 1642.50 (May 12) |

| Palm oil | Ringgit/tonne | 3421.00 | 2436.00 | 4506.00 (May 12) |

| Raw sugar | Cents/pound | 17.24 | 11.84 | 18.10 (May 11) |

| Coffee | Cents/pound | 153.40 | 97.80 | 162.35 (May 31) |

| Skim milk powder | US$/tonne | 3356.00 | 2609.00 | 3447.00 (May 18) |

| Cotton | Cents/pound | 94.95 | 68.00 | 98.50 (Feb 24) |

| Rubber | US$/100 kg | 204.40 | 152.50 | 272.40 (Oct 28) |

Note: Wheat, corn and soyabean prices refer to the most actively-traded futures contracts at the Chicago Board of Trade. One bushel equals 27.2155 kg of soyabean and wheat and 25.40 kg of corn. Raw sugar and coffee prices are for the most actively-traded futures at the Intercontinental Exchange. Skim milk powder price is the average at the fortnightly Global Dairy Trade auctions. Crude palm oil price is for the most actively-traded futures at the Bursa Malaysia exchange. Rubber price is for RSS-4 grade at Bangkok. Cotton price is the average based on the Cotlook ‘A’ index.

The second factor that will determine the outlook for food inflation in India is the monsoon. While the rains were 74% surplus in May, the southwest monsoon season (June-September) has itself so far recorded 26% above-average rainfall. These should induce higher kharif crop plantings that have already taken off. But since production is a function of both acreages and yields, a great deal rests on the rains during July-August, when the crop reaches the vegetative growth stage. 2019 and 2020 were excellent monsoon years. A third successive good monsoon should effectively put a lid on food inflation. That would be even more so if farmers expand acreages under oilseeds and pulses, which looks quite probable given the current market prices.

A third factor is the impact of fuel cost increases. The scope for their pass-through to consumers is today limited in an overall demand-constrained environment. Take milk. Dairies incur cost for its transport, first from the village collection centres to the processing plants that generally takes place in 2,000-3,000 litres mini-trucks. The milk that is pasteurized and packaged is further dispatched from the plants to the markets in bigger 10,000-15,000 litres tankers. Most dairies haven’t raised pouch milk prices, despite diesel costs going up by over Rs 15/litre in the last one year alone. What many of them have, however, done is reduce the prices paid to farmers. In Maharashtra, for instance, procurement prices of cow milk containing 3% fat and 8.5% solids-not-fat have fallen from Rs 31-32 per litre in February-March (pre-second wave) to Rs 21-25 now. In other words, the fuel pass-through has happened not by revising upwards the prices to consumers, but by lowering the prices paid to producers. In the event of a general growth and demand revival – whenever that happens – we could see processors, transporters and even farmers passing on the increase in fuel costs to consumers.

To the above three likely determinants, one may add a fourth, which is political. The Modi-1 administration’s tenure was marked by hawkishness on food inflation and privileging consumers over producers. During Modi-2, there has been focus on expanding minimum support price-based procurement, with new records in government purchases, particularly of wheat and paddy, getting established. Some of that has been prompted by the farmer protests against the Centre’s three agricultural reform laws.

The upcoming state elections in Uttar Pradesh might elicit similar political response in respect of sugarcane, where the minimum price payable to growers has hardly been revised during the four years of the Yogi Adityanath-led administration. How much of sugar price increase would the Modi government allow, in order to enable mills to pay more and on time to cane farmers? These are the kind of questions it may have to confront in other crops too, where the domestic supply-demand balance and international price environment are also more favourable to producers than a year ago.

Find all previous notes as part of the series here:

- Can rural play “savior” again? Agricultural seasons and COVID-19 waves by Mekhala Krishnamurthy and Harish Damodaran

- How ‘food’ has become the real social safety net in pandemic by Harish Damodaran

- Has MGNREGS Helped the Rural Economy in 2021? by Yamini Aiyar, Avani Kapur and Harish Damodaran

- Employment U-turn: Rural India is India’s main employer by Harish Damodaran and Yamini Aiyar

- Agricultural Households and Farming Income: An initial analysis of variations in income from farming and other sources among agricultural households in India by Harish Damodaran, Mekhala Krishnamurthy and Samridhi Agarwal

- Carbohydrates to proteins and back: How dietary and cropping diversification seems to have gone into reverse by Harish Damodaran, Mekhala Krishnamurthy and Samridhi Agarwal.

- Mapping India’s livestock economy by Harish Damodaran and Samridhi Agarwal.

- Unlocking the potential of Ganna Pradesh

- The Future of MSP by Harish Damodaran

- The Return of Food Inflation: Why its Different this time by Samridhi Agarwal and Harish Damodaran