Summary

The YouGov-Mint-CPR biannual surveys are conducted by Mint in association with YouGov India and Centre for Policy Research. This collaboration began in 2018 with the aim of assessing the beliefs, choices and anxieties of India’s young urban population.

The 12th round of this survey was conducted in July 2024, with 10,314 respondents across more than 200 towns and cities. In this latest round, 45% of the respondents were post- millennials (born after 1996) and 39% were millennials (born between 1981 and 1996).

In the last few months, the findings from this 12th round were published in Live Mint in a seven part series. Four of these articles were authored by Rahul Verma (Fellow, CPR) and Melvin Kunjumon, and have been summarised below. The full survey is linked here.

Polls and Perceptions: The 2024 Lok Sabha Election

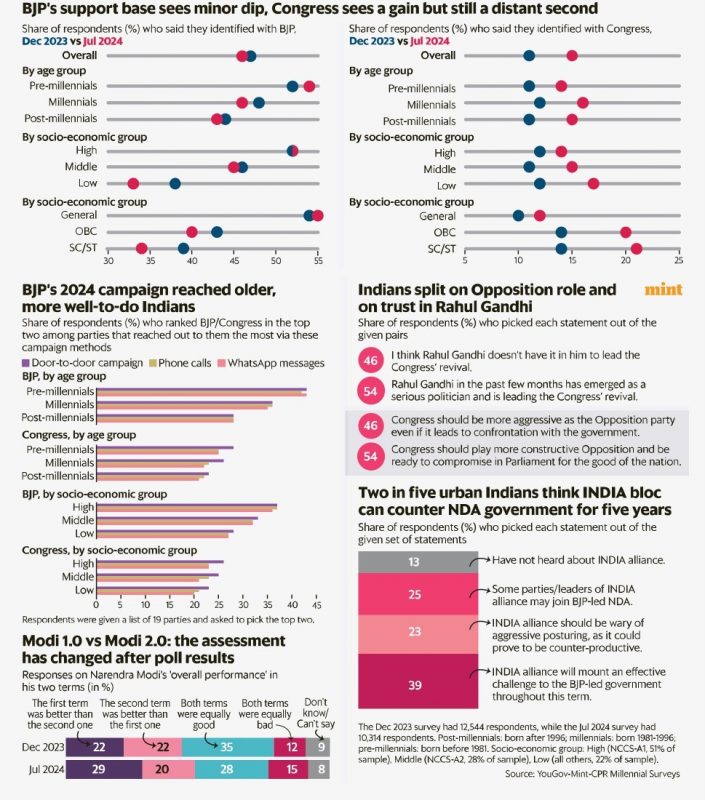

The findings of the 12th YouGov-Mint-CPR Millennial Survey conducted in July 2024 found little change in BJP’s approval rating in urban India with 46% respondents choosing it as their most favoured party, while Congress trailed at 15%.

The BJP garners its lowest proportional support from economically disadvantaged groups, and scheduled castes and tribes. In terms of voter outreach, the BJP fared better (with one-third respondents responding positively) than Congress (reaching slightly less than a quarter respondents).

On Rahul Gandhi’s emergence as a serious opponent, slightly more than half the respondents reacted favourably. When asked about the INDIA bloc’s ability to mount an effective challenge to the BJP in the incumbent government, about two-fifths responded in favour as against 29% in December 2023. The data suggests that the BJP’s public appeal has weakened among the lower socio-economic strata and that Modi’s popularity may have peaked.

Democracy Check

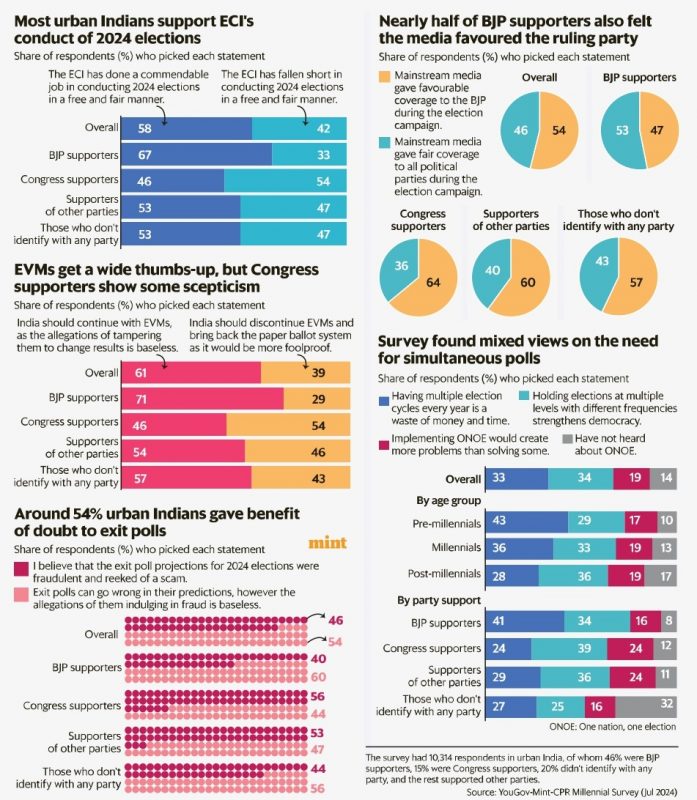

The second set of findings deals with determining the people’s faith in the electoral machinery. When asked about the fairness of the 2024 Lok Sabha elections, 58% people confirmed their faith while 42% responded negatively. A significant number of respondents, about every 3 in 5, supported the continued use of EVMs dismissing the allegations of rigging.

On being questioned whether the media gave favourable coverage to the BJP during its election campaign 54% respondents agreed, while 46% believed the coverage was fair. Surprisingly half the surveyed BJP supporters also affirmed that the media favoured the BJP. 46% respondents questioned the integrity of exit poll projections and claimed that the forecasts were fraudulent.

One-third respondents maintained that holding multiple elections was unresourceful, while another one-third held that staggered elections strengthen democracy. 41% of BJP supporters viewed multiple elections as wasteful, against only 24% of Congress supporters.

The survey findings are indicative of how party affiliations shape popular perceptions on electoral issues. BJP supporters exhibit greater trust in ECI, EVMs and exit polls, while Congress supporters are more likely to be skeptical.

Social Media and Politics

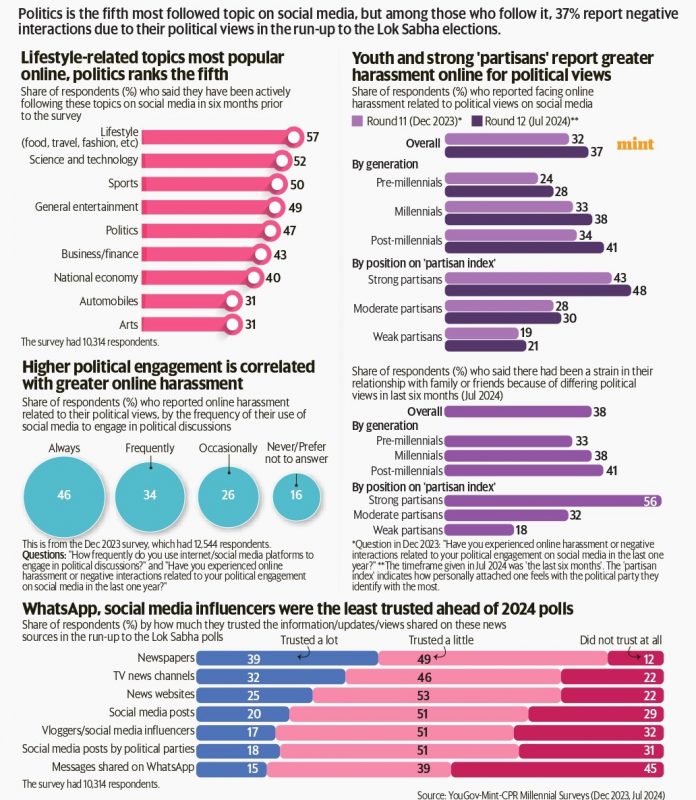

Another data set found that Politics was the 5th most popular topic on social media among respondents after Lifestyle, Science and Technology, Sports, and General Entertainment.

Similar to the previous round (conducted in December 2023), educated younger respondents with high incomes and strong partisan leanings tended to be more active in political discussions on social media. However, the latest round conducted right after the 2024 Lok Sabha elections, found an increase in negative interactions online, with the sharpest increase among post-millennials, from 34% to 41%. Respondents belonging to minority groups were more likely to report online harassment.

The respondents also showed a trust deficit in social media influencers and posts along with Whatsapp messages for information. Newspapers were the most trusted, followed by TV channels.

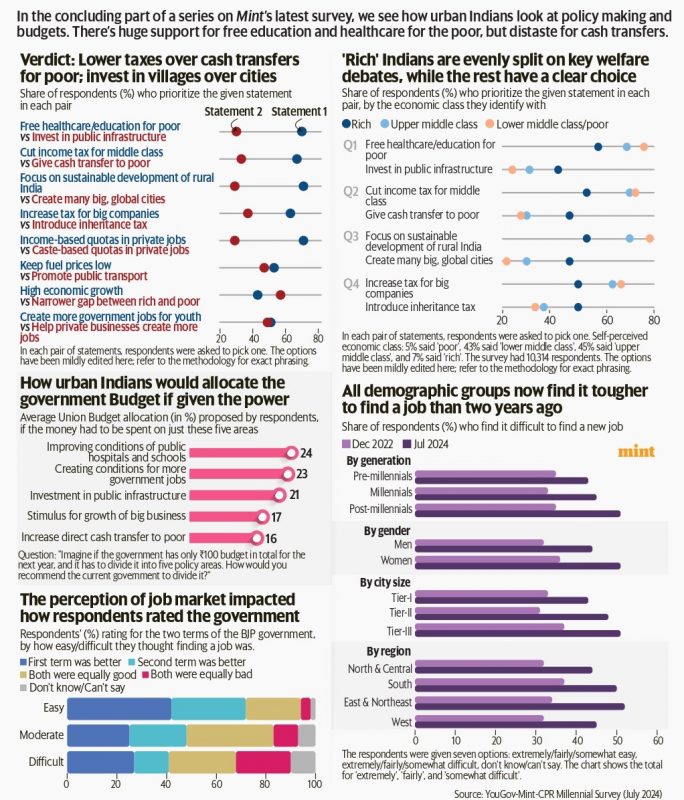

A Welfarist Budget?

The concluding survey focused on understanding the opinions of urban Indians on governmental budgetary priorities. The survey asked respondents to give their preference from paired policy questions. 70% participants favoured investment in free healthcare and education for the poor over public infrastructure, and prioritised rural development to building big, global cities.

To gauge these preferences, the survey asked respondents to allocate a hypothetical government budget of 100 Rs. across public hospitals and schools, creation of government jobs, investment in public infrastructure, growth of big businesses, and direct cash transfers to the poor. The results showed that respondents least preferred cash transfers and were the most favourable to improving conditions of governments schools and hospitals.

Finally, the survey also tried to assess whether people associate personal economic anxieties with the performance of the government. To the question of whether it is harder to find jobs across demographics, respondents reported that compared to the survey conducted in December 2022, finding jobs was harder in 2024.