Setting the context for state electricity regulatory agencies in India

Electricity is a concurrent list subject, with a federal dimension in the sharing of power and responsibility between the Centre and States. This reflects in the structure of electricity regulation in India. The Central Electricity Regulatory Commission (CERC) regulates tariffs for generating companies owned or controlled by the Central Government, those with an inter-State dimension, and those concerned with inter-State transmission of electricity. The State Electricity Regulatory Commissions (SERCs) regulate tariffs for generation, supply, transmission and wheeling of electricity within the States.

State Electricity Boards (SEBs) were set up by the Electricity (Supply) Act, 1948 to oversee generation, transmission and distribution activities. These were the backbone of the electricity infrastructure, and controlled 70 percent of electricity generation and almost all distribution by 1991. State governments performed the tariff-setting role. The decision on electricity pricing was often made with political considerations, and this led to a sharp deterioration of the financial condition and management practices of SEBs. A failed attempt to privatize the sector in 1991 was followed by a World Bank-supported reform effort in the state of Orissa, organized around unbundling and privatization in the sector. Several states followed in its steps, and in 1998 the Ministry of Power did the same through the Electricity Regulatory Commissions Act, 1998.

The CERC and SERCs were set up under the 1998 Act (later reconstituted under the Electricity Act, 2003) with the objectives of depoliticizing the sector and incentivizing private investment. The Electricity Act, 2003, designed to consolidate the various laws governing the electricity sector, brought in two key changes: (i) generation was delicensed; (ii) SEBs were to be ‘unbundled’ or separated into uni-functional utilities.

State in focus – West Bengal

The West Bengal Electricity Regulatory Commission (WBERC) was constituted in January 1999, under the Electricity Regulatory Commissions Act, 1998. It later came under the purview of the Electricity Act, 2003. The WBERC regulates the generation, supply, transmission, and wheeling of electricity (wholesale, bulk, and retail) within the state. It regulates power purchases and procurement processes, issues licenses, and determines tariffs for electricity operations in the State. The Commission also specifies and enforces standards with respect to quality, continuity and reliability of service by licensees. It is responsible for adjudicating disputes between licensees and distribution companies. Consumer grievances are addressed at the level of the utilities or the licensees. The Electricity Act stipulates that forums for redressal of consumer grievances be set up by all licensees. Consumers whose grievances are not settled by this forum or those who are aggrieved by the decision of this forum can approach the Ombudsman appointed by the State Commission. The WBERC primarily has a standards-setting and policy advisory role quite similar to the CERC, but limited to the state, and is bound to follow national electricity and tariff policy in the discharge of its functions.

As per Section 82 of the Electricity Act, a State Commission shall consist of 3 members, including the Chairperson. All members of the Commission are appointed on the recommendation of a Selection Committee chaired by a judge of the relevant High Court, and comprising the Chief Secretary of the State, the Chairperson of the Authority (for the selection of a member) or the Chairperson of the Central Commission (for the selection of the State Commission Chairperson).

These comments are being submitted in response to the ‘Notice for Public Consultation’ dated 30.06.2022 issued by the Ministry of Environment, Forest and Climate Change (MoEFCC) inviting comments/ suggestions on proposed amendments to the Air (Prevention and Control of Pollution) Act 1981 (Air Act).

The regulatory framework governing air quality in the country needs to be reformed urgently. Significant parts of the Indian population are exposed to air quality that does not meet the National Ambient Air Quality Standards. This crisis of poor air quality is neither urban-centric, nor seasonal, and its impact on public health is staggering. Apart from respiratory and cardiovascular diseases that are commonly associated with air pollution, it is also associated with diabetes, cardiovascular disease, adverse birth outcomes, and ocular conditions, and emerging evidence shows it may lead to other adverse health outcomes like dementia and neurodevelopmental disorders.

Many aspects of the regulatory framework need to be reformed or strengthened to appropriately deal with the nature and scale of the air pollution crisis. One of the key aspects is the ability of the regulatory agencies to enforce the law. Their failure in effectively doing so – evident from the poor quality of air experienced in most parts of the country – is attributable to various factors including institutional constraints, poor monitoring capacity, misalignment of statutory objectives and stated policy goals, and flawed legal design. The proposed amendments are limited to only one factor – the design of the Air Act in terms of punishments for offences.

To the extent the proposed amendments introduce monetary penalties per se for certain offences under the Air Act, the amendments are a welcome move. However, in our opinion, the proposed amendments need to be withdrawn and reconsidered for primarily two reasons: first, they are legally untenable due to excessive delegation of essential legislative functions; and second, the proposed regulatory framework, that will include Adjudicating Officers with the power to impose financial penalties, does not appear to be well-equipped to deal with violation of the law and its impact. Apart from this, there are several errors and inconsistencies in the proposed text which make its implementation problematic.

Our comments are divided into three sections. Section I discusses why the proposed amendments are legally untenable; Section II discusses why the proposed institutional framework will not reduce violations of the law; and section III lists some of the errors and inconsistencies in the text of the proposed amendments.

The State Capacity Initiative at the Centre for Policy Research (CPR), the Forum of Indian Regulators (FOIR) and the Indian Institute of Corporate Affairs (IICA) organised the following talk in the ‘Know Your Regulator’ talk series:

‘Know Your Regulator’: Mr Debasish Panda, Chairperson, Insurance Regulatory and Development Authority of India

In Conversation:

Mr Debasish Panda, Chairperson, Insurance Regulatory and Development Authority of India

Dr KP Krishnan, Honorary Research Professor, CPR

Dr Abha Yadav, Associate Professor, IICA and Director, FOIR

Dr Rohit Chandra, Assistant Professor, School of Public Policy, IIT Delhi and Visiting Fellow, CPR

The evolution of the insurance sector in India has three distinct phases –

1. 1938 – 1956: In the pre-nationalisation era, small and medium-sized insurance companies operated under the Controller of Insurance. This period is marked by considerable dissatisfaction among policy holders for not getting their dues on time. This was also a time where many mergers and liquidations took place. There were no clear regulations to protect policyholders.

2. 1956 – 2000: This era is marked by nationalisation. The Life Insurance Corporation (LIC) was nationalised in 1956 and subsequently, five non-life companies were nationalised in 1972. While policyholders’ interests were better protected in this era, growth was slow and there was little choice for consumers because of a rather monopolistic market consisting of four or five public sector companies.

3. Post-2000: The Malhotra Committee was set up and recommended a series of reforms for the insurance sector. IRDAI was given shape during this time. Initially, it was a purely regulatory body and at some point, based on Parliamentary committee recommendations, IRDAI was also assigned a development mandate.

In the era prior to liberalisation, there were several issues concerning policyholders and the slow growth of the sector. Specifically, these issues included a limited choice of products, costly products, low awareness and customer dissatisfaction regarding claim settlements. There were also issues with respect to the lapse of policies; term plans were not encouraged. In addition to these, there was also a limited spread of rural and welfare-oriented insurance.

The supply side was marked by a lack of competition because a lot of items were under tariff. In general, the lack of market discipline was witnessed. Professional standards in underwriting and risk management were not set. The aforementioned issues did not enable the sector to grow in an anticipated manner.

The IRDAI was set up with a clear mandate to protect policyholders and to ensure an orderly growth of the insurance industry. The liberalisation era witnessed the re-entry of the private sector alongside the public sector. Foreign Direct Investment (FDI) was allowed in the insurance sector. Companies also began listing during this regime. With such interventions, a number of companies came into the insurance market. In general terms, this is how the sector evolved.

The insurance industry also supports the economy in a huge way. The Assets Under Management (AUM) pump fuel into the economy by putting these resources into productive instruments for growth and development, promoting trade and commerce and promoting infrastructure development in the country.

Regulatory method: elements of executive, adjudicatory and legislative functions

Executive functions: Section 14 of the IRDAI Act casts a duty on the authority to regulate, promote and ensure orderly growth of the insurance and reinsurance business. This is done through a host of regulations. The Authority also issues directions, master circulars and guidelines. Through these means, the industry is regulated in an orderly manner, making sure that it is always in a position to honour the commitment made to citizens/constituents. The Authority also plays a supervisory role, as part of which it keeps a watch on the risk profile of insurance companies including whether they have maintained requisite solvency at all points of time, where the risks are sitting on company balance sheets etc. Crucial aspects such as these are constantly monitored through either an offsite mechanism or an onsite examination. It is through such mechanisms that the Authority tries to ensure the financial soundness of the company and its market contribution.

The IRDAI is also empowered to register and regulate the insurance entities. Once registered with the IRDAI, insurance entities are free to operate in the market, i.e. sell their products and service their clients. The Authority also approves changes in the shareholding, to make sure that risk is not concentrated in the hands of a few. The Authority also allows the issuance of other forms of capital other than equity or shareholders’ own money. The appointment and remuneration of the CEO and other corporate governance-related matters are handled by the IRDAI. This ensures that the entities are regulated in a proper manner.

Adjudicatory functions – Section 14(2) of the IRDAI Act empowers the regulator to adjudicate disputes between insurers and intermediaries or between the insurance intermediaries. It also provides powers to adjudicate and impose penalties, if required.

Legislative functions – The government frames the rules under the Act, whereas the Authority can frame regulations, as mentioned previously.

Role of the Central Government

The Central Government determines the policy framework, the broad guidelines and decides the sectoral focus that it wants. It is in charge of the statute and amendments made to the statute from time to time, depending on the needs of the citizens and the markets. Rules under the statute are framed by the government. It also appoints the Chairperson, other members and part-time Directors of the Authority. There are mechanisms where the Authority works closely with the government, for instance, the Financial Sector Development Council (FSDC), which is chaired by the Union Finance Minister. All the regulators are part of this forum, and inter-regulatory issues or issues that a regulator needs to flag before the government secretaries of the concerned ministries are discussed. This is an important and responsible committee which looks at issues pertaining to regulators including inter- regulatory issues.

Organisational structure

The Authority has a Chairperson with five full-time members and four part-time members. The city of Hyderabad is the headquarters for the IRDAI. It has two regional offices, one each in Mumbai and Delhi. There are close to 250 officers working in IRDAI. The Authority also has the flexibility of adding more personnel who may be recruited directly from the market at the level of assistant managers, through an all-India competitive examination and through an independent entity agency. There are officers in levels such as assistant managers and executive directors, who go up in the hierarchy through written examination and interviews. They also gain marks for the qualifications acquired through their course of service in the Authority. The Authority has professionals with wide-ranging experience, with qualifications in actuarial sciences, chartered accountancy, cost accountancy, law, engineering, technology and management. I think the organisation is rightly sized at present, but maybe as we go along we will add more layers of domain experts as required.

How IRDAI fulfils the objective of consumer protection

The essence lies in ensuring adequate access, affordability and fair value of insurance products for, both, prospective and existing policy holders. This has to be supported by necessary awareness, guidance and seamless servicing of claims. The third is a 360-degree framework which would include insurance, multiple distribution channels and service providers, academic institutions, data repositories and a network of ombudsmen (for speedy redressal of grievances). All of the aforementioned are in position to facilitate access, to service insurance and claim settlement process of the policyholders. The Authority has also framed the Protection of Policyholders Regulations, in 2017, which is applicable to all insurers, distribution channels and intermediaries, other regulators, and to policyholders. The broader objective of all this is: (i) policyholder-centric governance; (ii) fulfilment of obligations towards policy holders; (iii) best practices of sales and services of insurance policies in order to protect policyholders’ interest. Through these regulations, we have asked insurance companies to mandate a board-approved policy which would include the steps they are taking to enhance insurance awareness, service parameters including the turnaround time for settlement of claims, procedures they have established within their companies for expeditious complaint resolution, and the steps taken to prevent mis-selling and unfair business practices. They have also been mandated to display the service parameters and turnaround time prominently on their website for the benefit of consumers. The Authority also prescribed that certain essential data be provided in the insurance prospectus, for a prospective policyholder to read it and understand the scope of the benefits, the extent of insurance cover and the exclusions, policy conditions, and contact details of the insurer in case of the need for correspondence.

There is a concept of a free look policy, where the consumer can opt-out of the policy if it does not work for them. For a refund of the premium, the consumer can opt-out within 15 days if the policy was obtained physically, and can similarly opt-out within 30 days if it has been obtained online. Barring only the adjustments made for risk premium, and expenses such as medical tests or stamp duty, the consumer will receive a full refund. In case of a delay in refund, there is a penal interest of 2% above bank rate which the insurance company pays to the policyholder.

Nature of complaints made to the IRDAI

Generally, the complaints would be regarding settlement amounts being less than expected, mis-selling, delay in claims settlement, operational details about the policy etc. A host of such issues come up before the IRDAI from the policyholders. The Authority has now asked insurance companies to appoint grievance redressal officers. We are toying with the idea of having an internal ombudsman within the organisation, because a grievance redressal officer will have limited capacity to deal with complaints, whereas an internal ombudsman will perhaps be given a greater responsibility to settle the claim taking into account the policyholders’ complaints.

The IRDAI has also set up a portal called the Integrated Grievance Management System (IGMS), that acts as an interface between policyholders, IRDAI and the other entities (insurance companies and intermediaries). All complaints are registered in this System, and then sent to the insurance companies, after which the latter takes appropriate corrective action. This System is being analysed in detail, and we want to bring in data analytics to understand the number and nature of complaints, companies and their locations. Data analytics will help us identify the root cause of complaints and also take immediate corrective action.

We are also trying to revive the IGMS, which we now intend to call Bima Bharosa. This portal will be a more dynamic one and shall take care of customers’ needs in a time-bound manner. It will also take feedback directly from the customer, which helps in further improving the system. Thus, in the next couple of months we should have a more robust redressal system.

Key players in the insurance sector

The key stakeholders in the insurance ecosystem are insurers, policyholders, and intermediaries (about 40 to 50 lakh agents and entities). We periodically interact with all of them. We are trying to introduce an institutional arrangement to make these interactions more frequent, so that we understand the pain points that the industry is facing. The focus is on reaching out to every citizen in the country. The goal is to have a fully insured society – in order to do this, we are doing a gap analysis, trying to understand the current capacity and the number of additional companies and the capital to be augmented to existing players, whether distribution channels are working properly, their productivity, whether we need more technology-based solutions etc. All of these are on our drawing board. We are working to increase insurance penetration not only in terms of number of policyholders, but also the number of new policies issued.

Aspects of the insurance business that need regulatory scrutiny

The Authority has two roles to play: (i) a developmental role, where we need to ensure that insurance penetration, density and reach grows; and the (ii) regulation of financial soundness and market conduct of companies. We are trying to balance both such that the insurance sector grows in an orderly fashion.

Regulatory supervision is exercised on all relevant aspects – financial soundness, prudential norms, valuation of actuarial liabilities (existing and future), matching capital requirements, maintaining solvency at all points of time (since one does not know when the risk is going to unfold). All these aspects are factored through our prudential norms. How do we do this? This is done through onsite and offsite supervision, monitoring and overseeing various periodical returns and submissions that the insurance entities provide to the Authority, inspections (onsite) by a team of officers from IRDAI, regulatory actions wherever required (through issuance of directions, advisories, show cause notices and imposition of penalties).

As far as investment of assets (aggregated through policyholders’ money) are concerned, the IRDAI has a set of regulations on how such money is to be invested – some of this is in the statute and some are in the regulations we issue. Together, these give us an insight into how insurance companies are doing in terms of their investment returns, solvency, capital matching with the business they underwrite.

Regarding the governance issue, positions like CEO, CFO, Chief Actuarial Officer, Chief Distribution Officer, Chief Risk Officer, are critical in addressing the issues that we are concerned with. Currently, the IRDAI uses a traditional method of looking at risk factors – we are trying to move towards a risk-based supervision framework which will be enabled by technology. Within the IRDAI, we have created a vertical which is working on mission mode and engaging with industry so that we move hand-in-hand. We are also trying to move away from the factor-based method of considering solvency, towards a risk-based capital framework. There are countries which use a risk-based capital regime. We have a dedicated vertical working on this, engaging with stakeholders and building the technology required for this. The risk-based supervisory framework is expected to be ready in six to nine months, and the risk-based capital regime is expected to take two to three years’ time.

Challenges faced by IRDAI in regulatory enforcement and possible solutions

Enforcement is required when compliance is not up to the mark. Currently, a lot of supervision is compliance-based, but the risk-based supervisory framework is a much more potent tool. We have a lot of rule-based regulation here – with the industry maturing, we want to move away from rule-based to principle-based regulation. The principle gives bandwidth to the insurance companies and other stakeholders to operate within that framework. The regulator then does not need to specify each and every thing. For example, until now, every product to be launched by the insurance company needed prior approval of the regulator. We have now done away with it because the industry is mature and knows what price to set based on actuarial calculations (done by actuaries who are certified by the IRDAI). We have asked them to have a board-level policy for product certification – this will create internal checks and balances. After this, the regulator will obviously monitor how the product behaves in the market and what traction it gets, what complaints it receives on the product, and so on. As such, consumers have more choice now since companies can come up with more innovations and launch their products on-time without being delayed by the regulator. All health and non- life products do not need prior regulatory approval, except for the category of small ticket policyholders. For life products, we have given away all term-policy covers. Prior approval is still needed for long- term savings and pension products, but this will be further liberalised.

Through technology, a lot of offsite enforcement and monitoring of deviations can be done. We are also looking at newer tools. For example, through the IGMS website, which we now call the Bima Bharosa, we will get a lot of feedback on whether compliance is happening despite the regulations being in place. Thus, this newer regime that we are moving towards will see a lot of issues being resolved through the use of technology and data. Data is crucial for (i) proper pricing, which will give consumers better choices; (ii) processing of claims; and (iii) designing products that are more personalised. In order to address this, we have a repository or transactional data bureau called the Insurance Information Bureau (IIB). This is not optimally functioning, hence we are focusing on reforming the body into a professional body comprising people with the requisite background and expertise (for instance, a chief data scientist, a chief technology officer, CEO and so on). This body is probably going to be industry-led, with the regulator having an oversight function – because this data is most useful for the industry for appreciating and processing claims, which ultimately benefits the customer. This service should also come up in the next few months.

Professional organisations that IRDAI regulates

Typically, we do not regulate these organisations, but there is some kind of an oversight – otherwise, these are all self-regulatory bodies.

The most important one for us is the Institute of Actuaries in India because actuarial sciences is critical to insurance. It is a self-regulatory body but we have a representative on the Board who tries to bring up issues faced by the insurance sector. Some time ago, the insurance sector was struggling to find actuaries, but with efforts taken through IRDAI representatives and adequate steps taken by the government, there is now a reasonable supply of good actuaries in the country. In fact, a host of young people who joined IRDAI as engineers or management graduates have now acquired the actuarial qualification.

We are also closely associated with the Institute of Chartered Accountants of India (ICAI) and the Institute of Company Secretaries of India (ICSI). There is another professional body called the Indian Institute of Insurance Surveyors and Loss Assessors (IIISLA) which we associate with. As far as the councils are concerned, the General Insurance Council (GIC) and Life Insurance Council (LIC) are represented largely by insurers and other stakeholders (some nominees are from IRDAI and some from the government). These bodies are expected to take up issues concerning their respective industries, stakeholders and policyholders. While these two councils have existed for years, we discovered a lack of professional approach to bring up issues. We have recently met with the Chairpersons of the bodies and asked them to bring in more experts and knowledge partners so that they not only look at issues faced by the insurance companies in the country but also learn from international best practices. These councils can come up with papers to the IRDAI on a continuous or periodic basis so that we as a regulator are alive to the problems faced by them and can take care of them in a manner serving the larger interests of the sector. We are working to make these councils more professional, vibrant and robust so that they can complement and supplement our efforts and be responsive to the needs of the industry. The councils have already started that process – I recently saw an advertisement for a CEO with market-driven salary.

Capacity building in IRDAI

Every organisation needs some amount of capacity building since market trends change over time and new market instruments emerge. With the advent of technology, these challenges will be greater and we need to be alive to that. At IRDAI, I would say that we have a good amount of expertise in finance, actuarial science, management, technology and risk management, however, capacity augmentation and development is a continuous process. We have a series of programs for capacity building by way of training of people within the country and abroad to acquire domain expertise. We make it free of cost for people to acquire the requisite skill set. At the same time, we mandate some of the training that people must undergo. We are trying to build capacity in four areas– (i) risk-based supervisory framework; (ii) risk-based capital regime; (iii) human resources; and (iv) IFRS and IndAS.

Emerging technologies in the insurance sector

I recently met more than 200 players in the Insurtech world in Bangalore – there were interactions, presentations and roundtable discussions, and this ecosystem is raring to go. At IRDAI, we have already developed a regulatory sandbox mechanism where the proof of a concept is being allowed to be tested on the ground. We have found that the regulatory sandbox has certain shortcomings, for instance, currently, an applicant can only apply in two cohorts. We are revamping the system to make it a continuous process. Earlier, we allowed applicants to test their product for up to six months, now we are proposing to expand that to three years particularly for life products. Thus, we are working on a dynamic regulation that shall come up in the next few days. With new insurance technology coming in, we need to build capacity to regulate them in a manner that they do what they ought to do in terms of market conduct.

Finally, we are looking at allowing smaller players in the market. The penetration of banking in this country has happened through differentiated players. Similarly, for insurance, we are looking at micro-insurance players – niche players and regional players – coming into the segment. This will entail amendments to the Act, to allow companies with lesser capital to enter. However, it will help us with the objective of insurance penetration in unserved and underserved areas in the country.

Consumer protection issues and how IRDAI is addressing them

The IRDAI is reviewing existing systems, and trying to make them more responsive and robust. We are working on root cause analyses, on bringing in other forms of technology like robotic process automation, and so on. We are running a hackathon (shortly) where we will state these problems and how to resolve them using technology.

Bima Bharosa portal will become more vibrant, robust, responsive and take care of many issues. For the ombudsman mechanism, we have tasked the responsibility with an insurance ombudsman committee, where we have experts being led by a former Additional Chief Secretary level officer from the IAS. We are also contemplating an internal ombudsman within insurance companies.

We are trying to make disclosures furthermore in the larger interest of the policyholders. They ought to have more information to make a choice of what kind of policy to buy. Claim servicing and settlement is also something we will focus on very closely as far as turnaround times are concerned. All of this will need to happen on a technology platform. Hence, we are mainstreaming technology and incentivising adoption of technology in our regulations (which is expected to be out in a month’s time). The policyholder remains at the centre of our framework, and we are working to ensure that grievances do not arise, even if it means changing the terms of policy.

Views on regulatory convergence and a larger reform of the financial sector

The FSDC will be a very useful forum. One example of a common regulatory issue is the KYC. There is no need to reinvent the wheel each time when the same KYC can be used by all regulators. I believe a new mechanism is being contemplated by the Department of Revenue – e-KYC Setu – a bridge between me, the customer and the UPI. The Central Registry of Securitisation Asset Reconstruction and Security Interest of India (CERSAI) is another repository that has all the data. There is some element of concern with regard to the Prevention of Money Laundering Act (PMLA) where the last user of the CKYC data will have to update the information with regard to residential address, etc. which actually amounts to redoing the whole exercise once again. This is a concern that we will try to address in the next FSDC meeting. With the advent of new technologies, we should be able to take care of problems faced by the customer, whether they buy a financial, banking or insurance product. This forum is going to be important in addressing these concerns.

In terms of the reform of the financial sector, the IRDAI wants to move from rule-based to principle-based regulation. We have already delegated the product certification to insurance companies, and are considering some other things that the regulator currently does that can be delegated to the companies. We are looking at mainstreaming technology, a risk-based supervisory framework, risk-based capital regime, IFRS – these are some of the new reforms we have initiated and are trying to take forward.

We are also looking at value-added services to be incorporated in insurance. For example, a person aged around thirty five years would be reluctant to take health cover since they do not expect to go to the hospital in the next ten-fifteen years. Insurance companies can offer them services to make insurance attractive to this population segment – for example, offering a yoga membership, gym membership, an annual check-up, free ambulance service to their parents or nursing services – all of this should come in the bucket of value-added services.

The reason why insurance companies do not do this now is because the legal framework does not have clarity on this. As such, we need to carve out a space for these services. Further, a lot of capital will be required for companies to provide value-added services along with insurance because the same solvency norms will apply to them. If we can provide for them to set up a joint venture or a subsidiary and charge a fee for it rather than charging a premium, more people will be attracted to buying these kinds of insurance products. IRDAI is working on providing the technological platform for insurance companies to be able to provide these services.

Major disruptions that IRDAI is envisioning – the future of insurance sales

Technology is going to be the major disruptor. Everyone has to adapt to this sooner or later. We are nudging insurance companies to come up with a technology-backed insurance platform that they can create or their own or co-create or partner or collaborate on. A large number of players that want to enter the insurance sector are coming in with a technology solution. For instance, I found a crop insurance idea interesting – a parametric kind of insurance based on technology. Similarly, in the case of health insurance, for outpatient charges, there are concerns about frauds but a couple of players with technology solutions have already filed their applications on this subject.

Technology will be the enabler that allows reach to thousands of people at a point in time as opposed to the traditional agency network that only allows reach of two-four persons in a day. While we still need the agency network and some of the other traditional channels, we are nudging them to go down the technology route. Standalone digital players are now coming in, niche players have started filing applications, and as we go along, there will be a larger number of players backed by technology and end-to-end solutions. I expect them to come up with solutions that will compete with each other in terms of turnaround time for settlement of claims. Thus, technology would be the biggest disruptor and enabler in terms of customer satisfaction and reaching out to millions of people.

The key focus areas for us are as follows: (i) every life in this country must be insured – nobody should die without life insurance; technology will be crucial to achieve this goal, (ii) property insurance – people at the bottom of the pyramid (lower income segments and those who are calamity-prone) should be able afford property insurance cover, (iii) micro, small and medium-sized enterprises should be insured because there is a lot of potential in covering business risks and hopefully we will come up with solutions for this.

We constantly engage with the industry and have institutionalised bi-monthly meetings with insurance companies and other stakeholders, and open houses on the 15 th of every month. This is how we are looking to take care of disruptions.

Balancing public sector and private sector insurance

I think the market is so huge, innovations are so large and the scope is so broad that there is plenty of room for both public and private insurance to operate within the system. At IRDAI, we are completely agnostic about whether insurance offered is public or private. We want robust players with more capital so that they can underwrite more. The IRDAI has made the entry of new players absolutely seamless now – in a span of two Board meetings we are nudging them to come up with their final submission so that we can hand them a registration certificate to operate. In the past one and a half months, we have had more than twelve new applicants who want to start their own entity for insurance in India.

Financial independence of IRDAI

Financially, we are self-reliant. We do not need as much money to operate, but we put to good use whatever we have.

Risk profiles of individual entities

The risk-based supervisory framework and the risk-based capital regime are going to be game changers.

Balancing the commercial/market-related aspects of regulation with the more procedural aspects

The IRDAI is comfortable in balancing the expectations of the government, the public, the industry, the intermediaries and the professional organisations that are operating in this ecosystem. I view the regulator’s role here as one of a big facilitator apart from its supervisory role Some issues on which I plan to engage further with the industry includes how to facilitate growth of the sector by 15-20% CAGR or more, how to bring our insurance penetration closer to the world average in the next 4-5 years and then the G7 average. These are the aspirations we have at the IRDAI. Additionally, work that is underway includes putting in place more robust frameworks as far as prudential norms are concerned. The FSDC mechanism is another important platform for us to sort out a lot of issues which are inter- regulatory in nature. The insurance sector has tremendous potential, a huge market, and an increasing number of investors are looking to enter the sector. The policyholders will end up with a better deal as we go along, replete with more technology tools, better pricing, better underwriting, better claim servicing and processing.

The State Capacity Initiative at the Centre for Policy Research (CPR)’s talk series titled: ‘Know Your Regulator’ is held in collaboration with the National Council of Applied Economic Research (NCAER), the Forum of Indian Regulators (FOIR) and the Indian Institute of Corporate Affairs (IICA). In this talk series, we are talking to chairpersons and members of India’s regulatory agencies about regulation of Indian markets and the economy.

Our guest for the fifth event in the series was Mr. Supratim Bandyopadhyay, Chairperson, Pension Fund Regulatory and Development Authority (PFRDA).

He was in conversation with Dr KP Krishnan, Former Civil Servant and Dr Abha Yadav, Associate Professor, Indian Institute of Corporate Affairs and Director of the Forum of Indian Regulators (FOIR) Centre at IICA.

Mr Praveen Kumar, Director General and CEO of the Indian Institute of Corporate Affairs and Ms Arkaja Singh, Fellow, State Capacity Initiative, Centre for Policy Research made introductory remarks.

Date: 21st January 2022

The background note on PFRDA can be accessed here.

Conversation summary:

What were the problems that PFRDA was set up to address? How did it address these problems?

Serious conversation around the pension system, particularly the common pension system, started in mid or late 1990s. There were two reports – one by OASIS (Old Age Social and Income Security Project) and another by a High-Level Committee headed by Mr. B.K. Bhattacharya (senior civil servant) – that pointed out that the current defined benefit scheme is becoming unsustainable. The growth in pension bills, especially after factoring in defence pensions, were taking away large parts of revenue for both central and state governments. The political will of the leaders at the time enabled them to undertake strategic reform in the pension sector. Another thing that happened was the increase of 2 years in retirement age (58 to 60 years) in 1998.

The moment you go from an unfunded to a funded pension system (which is the basic difference between the earlier and the current system) – there has to be certain regulations, rules on fund management so that the benefits of employees are protected.

When we were planning this shift, we also thought about the unorganised sector, retail customers, and so on. So at that time, even though we started with the central government, and now all but two state governments have joined. Thereafter, we opened up to retail segment in 2009 and then to corporates as well. Today, the net addition from government sector has come down for obvious reasons while there is growth in contributions from the retail segment, corporates and unorganised sector. Hence, the purpose for which the PFRDA was set up is being fulfilled to a great extent, and unless we have platform to see that all subscribers, fund managers, data keepers are integrated, the purpose wouldn’t be served – hence we have ensured data security and robust connectivity between all intermediaries.

The PFRDA is a unique system because we work with 5-6 intermediaries, each of whom do different jobs. For example, pension fund managers only offer fund management service but don’t keep data. The PFRDA has a big role in ensuring the system works seamlessly and robustly.

Has PFRDA been pushed into a narrow box of looking after NPS, and should EPFO and other sectoral issues be brought under the PFRDA’s jurisdiction?

The birth of PFRDA was under some kind of a conflict – if you look at the pension sector, pension was already a part of IRDA’s domain and insurance companies are selling pension for over six decades. But pension is too serious a business to be left to different segments and regulators. There should be a single-point focus for pension.

Concerning gig workers, we had some discussion around a universal pension scheme, which has now received a mention in the Code on Social Security, 2020. This needs to be notified soon since gig workers really need pension today. Atal Pension Yojana is doing quite well, with 7 million new customers joining this year. While we are expecting around 10 million, the number we are actually looking at is 460-480 million, which is the number of people in the unorganised sector looking for some kind of old-age support. The question is: how do we reach out to them? There are self-managed superannuation products that don’t come under any regulator’s ambit. They get income tax approval and manage on their own. So we do not know whether contributions are made regularly, whether employee’s benefits are protected and if they get the right kind of payouts. So, in the long run, it will be prudent to place pension as a whole under one regulatory body.

Organisational structure of PFRDA

PFRDA is headed by a chairperson, and has three whole-time members (finance, economics, law). The board also has three part-time members, usually senior government officials nominated from the Department of Financial Services, Department of Personnel and Training, Department of Expenditure, and so on. We are supported by employees, all in the officer cadre. Currently our strength is 75-76 people, and we are in the process of recruitment. In two years’ time, we plan to have around 130-140 people, because certain activities like pension-related research, and we need separate inspection teams. We need presence in other regional centres, starting with Mumbai.

PFRDA currently has no independent or private members, but the PFRDA Act does not prohibit this. The three part-time members can be anybody, including experts in their fields.

Regulatory method: elements of executive, adjudicatory and legislative functions

PFRDA has all three functions: legislative, executive and adjudicatory.

Under Section 52 of the PFRDA Act, we make regulations for all intermediaries – pension fund managers, central record keeping agencies, trustee bank, NPS trust (trust structure that manages the assets on our behalf). The executive part is that we go for registration of entities, supervise and monitor their performance, audit and inspect them, determine their fees and charges. Through those inspections and monitoring systems, if we find breaches in regulations, we adjudicate under Section 30 of the PFRDA Act. We have the power to call for all their records, and if we find a breach we can impose penalties.

PFRDA has independence in these matters. Most of these decisions are with the board – the board is the final authority in this. The central govt comes into the picture to the extent that the benefits of central govt employees are concerned. For instance, three years back the government decided on the recommendation of the 7th Pay Commission to increase their contribution from 10 to 14%. Further, PFRDA has no say in the CCS and NPS Rules, which comes from the Department of Pension and Pensioners’ Welfare. Apart from this, the government does not interfere with PFRDA’s independence in the above-listed functions.

Main features of the terms of engagement set by PFRDA between savers and the sellers of pension products

NPS is a given product, pension fund managers manage funds on our behalf. Points of presence (POPs) are distribution channels of this given product. PFRDA tries to ensure that there is transparency in the system, to ensure that whoever comes into the system will know what the costs are like. NPS is probably the lowest cost financial product not only in the country but possibly in the world as well. We can say this because we engage with many international organisations of pension supervisors. IOPS looked at our overall cost structure and told us that we were outliers. We’ve also looked at lowest cost jurisdictions across the world and we are far below them. So we give low cost benefits, lots of information and data and lot of flexibility to the customers.

One important thing that came out in the High-Level Committee report was the issue of portability: govt employees who had not rendered a certain number of years of service wouldn’t get pension, and wouldn’t be able to transfer this either. The biggest advantage that the current system has is portability. Regardless of whether you are in the govt or private sector or on your own, you will have your unique account. You’ll just have to pay Rs.1000 annually to keep the account alive.

On the issue of sustainability, we aim to make the operation of intermediaries sustainable. At regular intervals, we look into their cost structures. For example, we have rationalised the cost structures of central record keeping agencies. Now we are looking at the cost structures of POPs. In order to take NPS and APY to the masses, we are telling POPs now that they can induct individuals into the system as well. In April 2021, we rationalised the fund management charges of the pension fund managers because they were running into losses. We have had 3 new licenses being granted for pension fund managers since then (we had 7 earlier). So it’s fair play between subscribers and service providers.

Who are the key players in this system beside the employer, employee and pension fund? What is the role of state and central goverments?

Each job in this system is done by a group of experts.

For example, we currently have 93 POPs – these are banks, NBFCs, and so on.

We also have retirement advisors, though this hasn’t gone quite well. Now we are going into individual players in the distribution market.

Central record keeping agencies (CRAs) keep the data of the customers, instruct banks (through which the money flows in) on which fund manager the money should go for investment. They are the central piece of the system. We currently have three – Protean E-Gov Technologies, KFintech and CAMS (they will start operation from next month).

We have a single trustee bank – Axis Bank – that manages the entire fund, right from the POPs and customers, to the pension fund manager, based on the direction of the CRAs.

Pension fund managers: There are 7 active ones and 3 licenses have been recently issued, so in the next 3-4 months they’ll be up and running.

Annuity service providers: Today, in the Act, the only way of exit is through annuity. You can take back 60% of your corpus tax-free and 40% has to be converted into annuity. This conversion process is tax-free of course, but the annuity is taxable. We have about 14 annuity service providers, all of them being IRDAI-conferred entities. We have been looking at other pay-out products as well, and it is part of our proposed PFRDA amendment bill. If it comes through, it will give a lot of options to the retiring public who are subscribed to NPS.

The nodal officers of governments are our intermediaries – they ensure that when the monthly salary is paid, the exact amount is deducted from the salary, and the contribution of the central/ state govt is added together and then sent to the system. Here, the biggest challenge we face is the delay: (i) not deducting in time; (ii) even if deduction happens, the money is not coming to the system in time. The system is very dynamic today: if you give the money today, it will get invested today itself; hence a delay of 20-30 days entails an opportunity loss. For the first time, in CCS-NPS Rules, a provision is brought in that if there is a delay there will be a penalty, including individual penalty. The proposed amendment bill also provides that the dues will be treated like any other statutory dues.

Justification for pensioners’ benefits being market-linked

Chairperson, PFRDA: The previous and the current pension schemes are not comparable at all. Firstly, no amount of contribution was required in the previous pension scheme. Secondly, retirement ensures a 50% replacement rate and is adjusted to inflation every six months, in the new scheme; recovery and wage rise with every pay commission also brings adjustments to old pension.

In a market-linked scheme, we monitor the performance of pension fund managers, we have strict investment guidelines with some scope for growth, and we ensure that they do not become too adventurous because these are retiree’s monies. Since 2009, we have managed the private sector as well, and over 13 years the CAGR under our equity scheme is 13.5%. Even corporate bond funds have given a CAGR of 9.72%, despite several corporate market events. The government bond performances are a little lesser, but that is around 9.3-9.4%, because the interest rates are hardening today. If you look over a period of time at blended return of an equivalent amount in equity, corporate bond and govt securities, it will still be over 10%. We have benchmarks in place and ensure that pension fund managers work close to them, and if there are huge deviations we hold them accountable. Financial markets have volatilities in the short term, but over a period of time we ensure that the right kind of securities are chosen for subscribers and they get a sizeable corpus.

Dr. KP Krishnan: This discussion takes us to the knife-edge job of the regulator, it is not the regulator’s job is not to ensure good returns to the subscribers but to ensure no malpractices and that the regulated entities act according to the prescribed behaviour, and a lot of the risks are to be taken by the informed investor. What you have brought out nicely is the difficulties in a pension situation where the choices are not necessarily exercised by the investor, so there is a dilution in the role of the investor, which then is performed by various actors.

On the issue of early withdrawals and annuitisation of the pension corpus: individuals tend to be less concerned about building a long-term corpus for themselves than society is. How much of this should be done by the regulator and how much of this should be done by educating the public and letting individuals take a call?

The biggest challenge with annuity is that once you enter it you are stuck for a lifetime, whatever the rates may be. Whatever we see today are fixed rate annuities. There is no variable annuities in the market; it does not move along the interest rate scenario. Currently the annuity rates are varying between 5-6%, and this is normally for those asking for annuity and after death for the corpus to be refunded to the nominee. In Indian psyche, 90% people go for this – they feel that after they die it is their duty to give the corpus to close ones, regardless of whether they need it or not. They choose to trade off higher annuities for getting the money right after death. This is a big challenge in the system today.

So far as exits are concerned, the biggest complaint against NPS is that it discourages early access to the funds. But after considerable deliberation, we now allow three times partial withdrawal (25%) for the same reasons that EPFO allows – for construction of house, marriage of children, meeting medical costs, and so on. Beyond this, we do not allow withdrawal because as we have seen with EPFO, early access being freely accessible leads to depletion of corpus, culminating in a situation where a person gets no corpus on retirement. Since the system is for old age security, a substantial part of the corpus should be left at retirement.

The ideal view is that individuals have different instruments for different goals – NPS is not ideal for instance for medical costs or housing, but in a developing country there will be competing claims on limited amount of savings. In this context, what is the NPS doing for greater education of its customers?

PFRDA has training agencies in place and are involved in online training. For annuities, retirement and related matters, we have annuity literacy programs. For the last 2-2.5 years, we had around 30 sessions, with physical sessions before the pandemic; in Patna for instance, we had 300 people inside the auditorium and 500 outside. People have asked if they can contribute post-retirement. Now these sessions are conducted online, where 70% of the session is dedicated to audience questions. We also bring in pension annuity service providers, CRAs, fund managers.

Apart from this, we are trying to create an industry body. The NPS trust is already trying to do that, by bringing together fund managers, CRAs, POPs to create awareness.

We are trying to have a resource person -like concept that SEBI also had, who will go around and talk about pension in general.

I also believe that pension, health insurance and life insurance should be taken together. By contributing to NPS, the corpus may go up but the person and their family are not protected – hence, it has to be a combination of all these things. I strongly believe that different regulatory bodies like IRDA and us should work together towards a common forum through which we can educate people about these things.

During my 35 years in the insurance industry, pension has never been a top seller – ultimately if someone is really insisting on a pension will the insurance company sell it. No agent or advisor will actively talk about pension – but pension is one of the very important segments but everyone should be talking about.

There are changing demographics, people have longer lives and fewer babies. Is this the context for necessary focus on the issue of pensions? Has this transition happened?

The life expectancy at birth in India is close to 69 years now, and life expectancy at 60 is another 18-20 years; female longevity is 2 years more than male longevity. So we have to start quite early to think about longevity. We do a lot of industry sessions with CII, FICCI and so on – and we get questions, mostly from people in their 40s and 50s, about how much they need to accumulate in 10 years’ time for their post-60 life. In most situations we see that it is too late by the time they are starting; but we encourage them to start anyway. NPS in that sense is a very flexible system, where a person can contribute just Rs.1000 a year to keep the account alive, when they have restricted cash flows, and when they have higher cash flows they can contribute more and secure what you need at the end of your life. Regarding replacement rate, take for instance, IT graduates aged 25 years having a salary of Rs.30,000 a month with an annual increment of 8%, with inflation around 5% – and they depend only on the mandatory benefits of provident fund and gratuity – their replacement rate will be around 25% of their last earned salary. This cannot be adequate given the biggest cost incurred post-60, i.e., medical costs. Morbidity experience – the quality of life after 60 or 65 – entails huge costs as the pandemic has shown us. This is why we need to be prepared since the longevity issue will catch up with us in a big way.

Now we have opened it up for the retail and corporate customers to continue after 60 years till the age of 75 years – they are free to close it any time in between and take their 60% money and go for annuitisation of 40%.

Regulatory capacity of PFRDA – staffing, technical expertise, etc.

The year 2021 was a turnaround year for the PFRDA since it became financially independent. We now run on regulatory fees and did not take a single budgetary grant to run our operations. This maintains our autonomy to a great extent. This helps us in recruiting people of our choice, improving our IT infrastructure and so on without depending on govt support. We have also set up a small fund to have our own office building.

We do not have any monetary constraint with regard to recruitment of capacity building and of experts. In our latest recruitment, we recruited actuaries for the first time, with the long term purpose of NPS being only one of many financial instrument with which the PFRDA will be working. Between 2004, when we were established, and now, NPS has changed its structure and shape quite a bit, since we added many flexibilities, but we need other kinds of products as well. The first thing we started, that was also given in the statute, is the Minimum Assured Returns Scheme (MARS). This again is very difficult in a market-linked scheme but we hope for the first basic product to be available in the next 6-8 months. It will look into many aspects – the moment you bring in the concept of assured returns in a market-linked scheme, we have to look at the solvency aspect of fund managers. Currently, I give them a fund and they give a certain kind of return net of their expenses. But if they are asked to give a certain kind of finite return regardless of market conditions, the concept of solvency comes into play – they have to be adequately capitalised. Once MARS is successfully implemented, we’ll be looking into other kinds of products. If the PFRDA amendment bill allows us to go into exit-related products, we’ll look into that – we have in mind a systematic withdrawal plan as an alternative to annuity.

Apart from actuaries, we are recruiting chartered accountants, cost accountants, company secretaries, economists, statisticians (for research), and so on. Our report from BCG, our consultant, looks into several aspects like operation of NPS trust, entire HR aspect of PFRDA and the areas that PFRDA should look into, kind of personnel PFRDA needs, and revamping of PFRDA’s IT infrastructure. This is a one-year project and these things are on the agenda.

Sources for principles, technical expertise and establishment of norms

We depend on three sources –

looking at other financial sector regulators and their best practices;

international practices – everything can’t be imported and immediately applied here, but we are working on that. For example, we are engaging with other countries on how they’ve made systematic withdrawal plans work; feedback from customers, intermediaries – we work with many CPSEs (central public sector enterprises) that are shifting their superannuation funds to us; here too we get feedback on what their employees want.

Climate Law and Governance as Indicators of ‘Ability’ to implement the Paris Agreement

Climate change laws and governance arrangements are important indicators of countries’ ability to implement the Paris Agreement and their Nationally Determined Contributions (NDCs). In assessing such ability, it is helpful to consider a set of key governance functions the presence of which can underpin successful domestic mitigation and adaptation efforts in the long term. These functions include: direction-setting, strategy-setting, coordination, integration, mainstreaming, knowledge-production, stakeholder-alignment, finance mobilisation and allocation/channelling, and oversight and accountability. Although these functions will be met through various legal and policy instruments depending on political context, climate change laws offer potential for the creation of institutions and processes that effectively embed such functions in ways resilient to changing political fortunes. Consequently, it is necessary to go beyond the numerical measurement of progress made as regards

emissions reductions, finance, and other such benchmarks, to more fully account for the collective ability to effectively address climate change in the critical decades to come. This can be achieved through a deeper understanding of current national legal frameworks and institutions, which can in turn serve as the basis for extrapolating best practices in domestic climate change governance.

Setting the context for state electricity regulatory agencies in India

Electricity is a concurrent list subject, with a federal dimension in the sharing of power and responsibility between the Centre and States. This reflects in the structure of electricity regulation in India. The Central Electricity Regulatory Commission (CERC) regulates tariffs for generating companies owned or controlled by the Central Government, those with an inter-State dimension, and those concerned with inter-State transmission of electricity. The State Electricity Regulatory Commissions (SERCs) regulate tariffs for generation, supply, transmission and wheeling of electricity within the States.

State Electricity Boards (SEBs) were set up by the Electricity (Supply) Act, 1948 to oversee generation, transmission and distribution activities. These were the backbone of the electricity infrastructure, and controlled 70 percent of electricity generation and almost all distribution by 1991. State governments performed the tariff-setting role. The decision on electricity pricing was often made with political considerations, and this led to a sharp deterioration of the financial condition and management practices of SEBs. A failed attempt to privatize the sector in 1991 was followed by a World Bank-supported reform effort in the state of Orissa, organized around unbundling and privatization in the sector. Several states followed in its steps, and in 1998 the Ministry of Power did the same through the Electricity Regulatory Commissions Act, 1998.

The CERC and SERCs were set up under the 1998 Act (later reconstituted under the Electricity Act, 2003) with the objectives of depoliticizing the sector and incentivizing private investment.

The Electricity Act, 2003, designed to consolidate the various laws governing the electricity sector, brought in two key changes: (i) generation was delicensed; (ii) SEBs were to be ‘unbundled’ or separated into uni-functional utilities.

State in focus – Kerala

In the year 1958, the electricity department of the Kerala State was converted into the Kerala State Electricity Board (KSEB), under the Electricity (Supply) Act, 1948. KSEB was responsible for generating, transmitting and distributing electricity within the State. Kerala is a land of mountains and rivers. As such, the region is conducive to the generation of hydroelectricity. In the 1980s, the state depended on a surplus supply of inexpensive hydroelectric power to attract energy-intensive industries. The KSEB even exported the surplus power to neighboring states to earn revenue. By the mid 1990s, however, there was a shortage of generation facilities coupled with growing demand. KSEB is understood to have turned into a net importer of electricity during this period. As a result, not only was the state deficient in power supply but also had to deal with KSEB’s financial burden.

In 2003, with the passage of the Electricity Act, the SEBs were required to be re-organised such that the key activities of generation, transmission and distribution of electricity could be undertaken by different entities. Under a mutual agreement with the Government of India, KSEB continued to function as a State Transmission Utility (STU) and distribution licensee until 2008. From 2008 to 2013, the state government took over the functioning of KSEB as per section 131 of the Electricity Act, 2003. Subsequently, the state government revested all functions, properties, interests, rights, obligations and liabilities of KSEB to its successor, a corporate entity named the Kerala State Electricity Board Ltd (KSEBL) which is a transmission and distribution utility.

The Kerala State Electricity Regulatory Commission (KSERC) was constituted in November 2002, under the Electricity Regulatory Commissions Act, 1998. It later came under the purview of the Electricity Act, 2003. The KSERC regulates generation, transmission, wheeling and distribution of electricity within the State. It regulates power purchases and procurement processes, issues licenses and determines tariffs for electricity operations in the State. The Commission also specifies and enforces standards with respect to quality, continuity and reliability of service by licensees. It is responsible for adjudicating disputes between licensees and distribution companies. Consumer grievances are addressed at the level of the utilities or the licensees. The Electricity Act stipulates that forums for redressal of consumer grievances be set up by all licensees. Consumers whose grievances are not settled by this forum or those who are aggrieved by the decision of this forum can approach the Ombudsman appointed by the State Commission. The KSERC primarily has a standards-setting and policy advisory role quite similar to the CERC, but limited to the State, and is bound to follow national electricity and tariff policy in the discharge of its functions.

As per Section 82 of the Electricity Act, a State Commission shall consist of 3 members, including the Chairperson. All members of the Commission are appointed on the recommendation of a Selection Committee chaired by a judge of the relevant High Court, and comprising the Chief Secretary of the State, the Chairperson of the Authority (for the selection of a member) or the Chairperson of the Central Commission (for the selection of the State Commission Chairperson).

Sectoral challenges

Kerala’s reliance on power purchases from other states in order to meet its needs imposes huge costs on the state exchequer. As per the 19th Electric Power Survey conducted by the Central Electricity Authority, the state’s energy consumption is projected to increase by 54% in 2026-2027. [1] With an ever-growing demand, the State may need to strategically diversify current sources of power generation. Long-term resilience in the State’s power sector will be dependent on harnessing the region’s unique topography and environmental features. The Kerala State Power Policy (2019) acknowledges that the State is facing issues related to the quality and reliability of power supply. A detailed assessment of the current transmission and distribution network may be necessary to identify nodes that require revamp.

Kerala’s electricity sector, much like the rest of the country, faces a combination of legacy issues and future challenges. There is a tendency to over-judicialize the field of regulation, which increases costs and tends to benefit financially stronger parties in legal disputes. Further, in terms of a future agenda for the sector, the State will need to explore Renewable Energy (RE) sources best suited for its conditions including the increasing occurrence of climatic events like floods.

As a regulator, KSERC aims to provide a level-playing field to the players in the electricity sector. Amongst the many interventions it has taken towards this, the Commission has released open access regulations to enable power consumers, especially those who consume large quantities of power, to access energy from sources of their choice using the linking network of transmission and distribution licensees. It has recently announced a revised tariff structure for the State. The last such revision took place in the year 2019. State regulatory commissions play an important role in defining the broad contours for the development and functioning of the electricity sectors in their States. An independent, consistent and forward-looking electricity regulatory regime will nudge States closer to achieving self-sufficiency, transition to newer and cleaner energy sources, and encourage an integrated development of the sector.

[1] Kerala State Planning Board, Economic Review, 2017, https://spb.kerala.gov.in/economic-

review/ER2017/web_e/ch52.php?id=50&ch=52; percentage increase projected as per energy consumption values in 2017-2018.

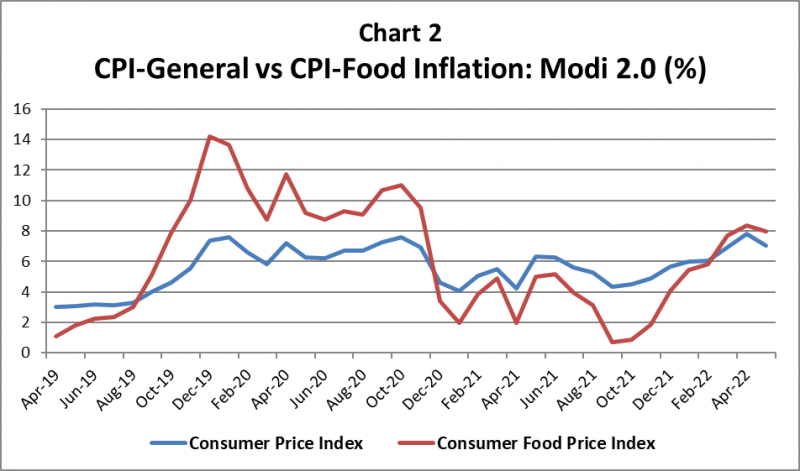

Since the start of this calendar year, annual consumer price index (CPI) inflation has ruled not only above the Reserve Bank of India’s (RBI) target of 4%, but even its upper tolerance level of 6%, for every month from January to May. If we take the 38 months from April 2019 to May 2022 – roughly coinciding with the Narendra Modi-led government’s second term (Modi 2.0) – CPI inflation has exceeded the 4% target in as many as 32 months and even the 6% ceiling in 18 months. This has been seen by many as a failure on the part of the central bank to adhere to its inflation-targeting mandate, enshrined in law since June 2016 (https://bit.ly/3b1JJbZ and https://bit.ly/3OcrDCp).

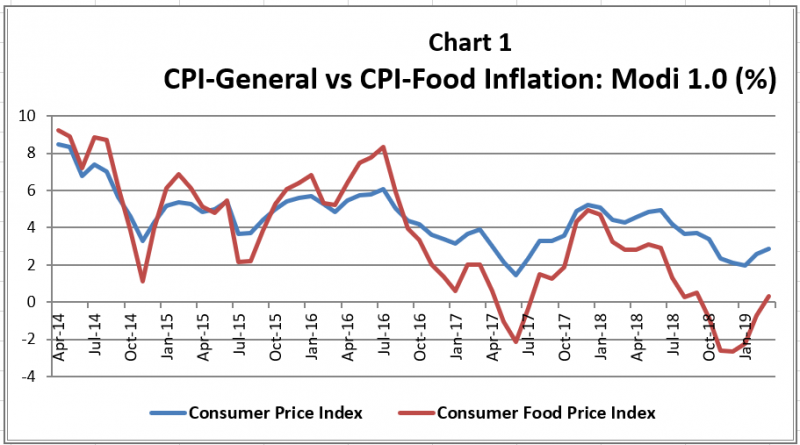

The above “failure” is in contrast to the “success” achieved in the Modi government’s first term (Modi 1.0). During that period, roughly from April 2014 to March 2019, the 6% ceiling was breached only in 6 out of the 60 months. Moreover, CPI inflation was contained within 4% in 23 out of the 60 months. A far cry from the 6 out of 38 in Modi 2.0, with even those six being in the first six months from April to September 2019!

But the story isn’t just about overall retail inflation. During Modi 1.0, year-on-year general CPI inflation averaged 4.49%. It was even lower, at 3.52 per cent, for the consumer food price index (CFPI) inflation, with the latter ruling below the former in as many as 38 out of the 60 months. In other words, while inflation in general was benign, food inflation was even more so. That trend was visible particularly after September 2016, as can be seen from Chart 1.

It’s been quite the opposite in Modi 2.0. Overall CPI inflation has averaged 5.59% during these 38 months, 1.1 percentage points higher than in Modi 1.0. No less striking is CFPI inflation, which has averaged even higher, at 6.21% or almost 2.7 percentage points more than during Modi 1.0. In 18 out of the 38 months, food inflation has exceeded general CPI inflation, while also exhibiting greater volatility, as Chart 2 shows. For both the government and RBI, food inflation has been the bugbear – due to greater political sensitivity and less amenability to control through monetary policy tools such as repo interest rate and cash reserve ratio hikes.

Imported inflation

A major source of the resurgent food inflation has been global prices.

During the Modi 1.0 period, these were low: International agri-commodity prices actually collapsed from around late-2014. The UN Food and Agriculture Organization’s food price index (FPI; base year: 2014-2016=100) averaged 131.9 points in 2011, which was at the height of the previous commodity boom/super cycle. The index fell to 122.8 in 2012, 120.1 in 2013 and 115 in 2014, before plummeting to an average of 93 and 91.9 points in the subsequent two years. The average annual FPI inflation during April 2014 to March 2019 was minus 3.95%, below even the corresponding Indian CFPI rate of 3.52%.

Again, it’s been the other way round in Modi 2.0, where global FPI inflation has averaged 13.42%, higher than the 6.21% retail food inflation in India over the 38 months from April 2019 to May 2022. Simply put, while low international agri-commodity prices helped control domestic food inflation during Modi 1.0 – even translating into depressed crop realizations for farmers – their soaring from around October 2020 has produced the opposite effect. The FPI crashed to a four-year-low of 91.1 points in May 2020 when most countries had severe lockdown restrictions in place. But with the post-Covid demand recovery and easing of lockdowns, the index rose to 135.6 points by January 2022. The Russian invasion of Ukraine on February 24 took it to an all-time-high of 159.7 points in March, from where it has marginally fallen to 157.4 in May.

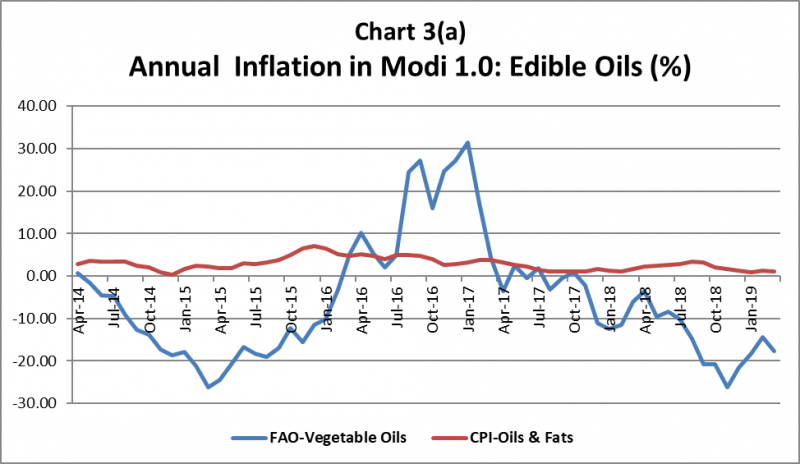

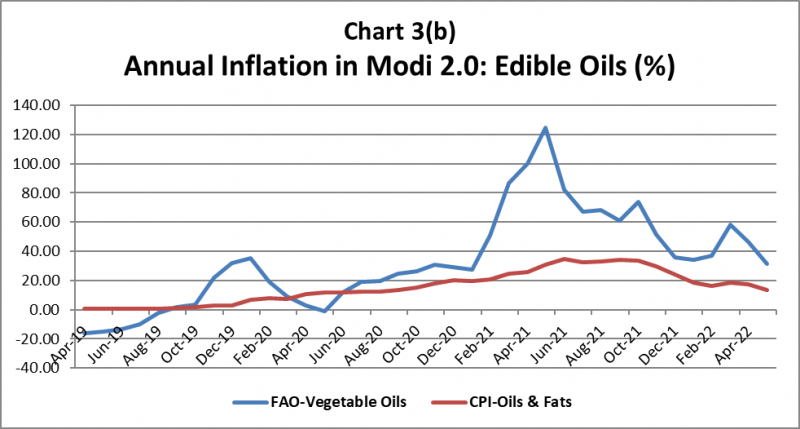

The transmission of international prices to domestic inflation in India is best illustrated by edible oils. During the Modi 1.0 period, average year-on-year inflation in the global FPI for ‘vegetable oils’ was minus 5.79%, while at 2.89% for the CPI in ‘oils and fats’. But in Modi 2.0, the former has averaged 33.31% and the latter 15.5%. Charts 3(a) and 3(b) plot the month-wise FPI and CPI inflation rates in edible oils for both periods. The correlation coefficient for international and domestic inflation is positive for edible oils: 0.33 in Modi 1.0 and 0.85 in Modi 2.0. Indian consumers benefitted from very low (almost flat) inflation during 2014 to much of 2020, whether in palm, soybean, sunflower, mustard and groundnut oil or vanaspati (hydrogenated vegetable oil). But as global prices of vegetable fats skyrocketed – for reasons we shall detail in the next section – consumers experienced sudden and sharp inflation in this commodity (https://bit.ly/3tBalqX).

There’s no such correlation, though, when it comes to cereals. Average annual inflation was low both for CPI in ‘cereals and products’ and FPI in ‘cereals’ – at 3.38% and minus 3.32%, respectively – during the Modi 1.0 period. In Modi 2.0, India’s CPI cereal inflation averaged even lower, at 2.6%. This was despite the average year-on-year global cereal FPI inflation shooting up to 12.81% during this 38-month period. Unlike with edible oils, the correlation coefficient for international and domestic inflation has been weak and negative in cereals – at minus 0.017 during Modi 1.0 and minus 0.40 during Modi 2.0. The reason for it has to do with government’s minimum support price (MSP)-based procurement and stocking of wheat and rice for channeling through the public distribution system (PDS). Maintaining more than adequate stocks in the Central pool, both for the PDS and open market operations, has effectively insulated Indian cereal prices from the vicissitudes of the world market. The PDS prevented inflation from being imported into India during Modi 2.0, just as MSP procurement ensured no cereal deflation during Modi 1.0.

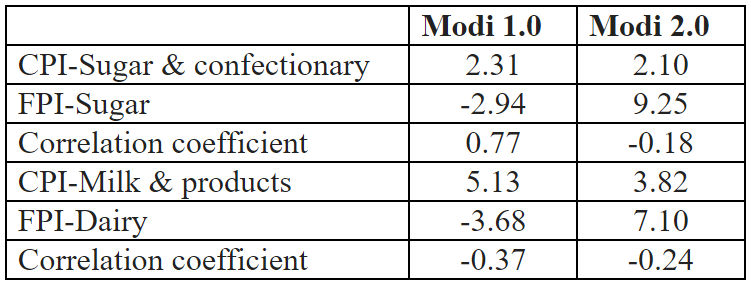

We have found similar results for sugar and dairy. As the table below shows, average CPI inflation has fallen for both during Modi 2.0 compared to that in Modi 1.0, even while rising significantly for the global sugar and dairy FPIs.

Sugar and Milk inflation: Domestic vs Global (% average year-on-year)

Low international sugar prices weighed heavily on realizations for domestic mills and, in turn, their ability to pay cane growers during a greater part of the Modi 1.0 period. But in Modi 2.0, high global prices helped Indian mills to export record quantities. At the same time, production being in excess of

domestic consumption requirements – which was the case for rice and wheat as well – ensured little CPI inflation in sugar. Production self-sufficiency, coupled with established systems of procurement and marketing by cooperatives and organized private dairies, has resulted in no imported inflation for milk and milk products either. The correlation coefficient between international and domestic prices has been negative and weak for sugar, dairy and cereals, while positive and strong in edible oils during Modi 2.0. Inflation from import dependence and the resultant transmission of international prices has been a factor for pulses too. Average CPI inflation in pulses was only 4.29% in Modi 1.0. It has more than doubled to 10.31% during Modi 2.0. Pulses imports peaked during 2015-16 to 2017-18, averaging over 6 million tonnes (mt). In the last three years, imports have more than halved to about 2.7 mt, but they are still significant relative to domestic production of 24-25 mt.

Structural versus idiosyncratic inflation

Food inflation isn’t new to India. Average annual inflation in the wholesale price index for ‘food articles’ was 10.21% during the previous UPA regime from 2005-06 to 2013-14. That inflation, though, was structural and demand-led, driven by growth in incomes, including of poor and lower-middle class households. Rising real incomes, as a previous note in this series has shown (https://bit.ly/3nheUTP), also contributed to significant dietary diversification, with per capita consumption of foods rich in proteins, vitamins and minerals (milk, egg, meat, fruits and vegetables) going up and that of carbohydrates/calories-based foods (cereals and sugar) declining. A byproduct of it was what the former RBI deputy governor Subir Gokarn termed “protein inflation”. In a late-2010 paper (https://bit.ly/3N4vEb0), he wrote how “increasing demand for proteins appears to be an inevitable consequence of rising affluence”, while warning of persistent demand-supply balances that would make pulses, milk, eggs, fish and meat relatively costlier down the line.

The current food inflation, on the other hand, is more idiosyncratic and supply shock-driven, rather than structural. We have already noted that retail inflation in milk and milk products has fallen during the Modi 2.0 period. Annual growth in milk sales by cooperatives, too, has averaged just over 3 per cent from 2014-15 to 2020-21 (National Dairy Development Board annual reports). Low price increase and sales growth in milk – a product with very high income elasticity of demand in India (https://bit.ly/3HyTlHA) – is indicative of no major “structural” drivers and the return of food inflation being attributable mainly to “supply-side” factors.

The last two years and more have witnessed four kinds of supply shocks – from weather, export controls, pandemic and war.